<script src="/assets/frontend/govuk_publishing_components/vendor/lux/lux-measurer-d66192b1b665d415e1874e49a48138b7ae339548aa6cdb8687c7f9933e72b969.js" async="async"></script>

<script src="/assets/frontend/govuk_publishing_components/rum-custom-data-b9e1806d1da2fa8ef1855d01aa71ba5eb0afc010dd2c4de3672cc7c7a39b0c8c.js" type="module"></script>

<script src="/assets/frontend/govuk_publishing_components/rum-loader-a65b10e18ceeba3bd8a2eac507c7f2c513cdc82f35097df903fdea87f1dc2e33.js" async="async" data-lux-reporter-script="/assets/frontend/govuk_publishing_components/vendor/lux/lux-reporter-16e474d53ab9842457c92448e9ea0e6faea553d7b8250f940eec8c50285b48af.js"></script>

<meta name="govuk:components_gem_version" content="65.1.0">

<script src="/assets/frontend/govuk_publishing_components/load-analytics-c0b21edf0d79bd3dd6172b0c5be4dfd3c073a8aab9275e31253be3a26762c9a9.js" type="module"></script>

<meta name="csrf-param" content="authenticity_token" />

<meta name="csrf-token" content="GvRVdQlvdLPn0Mju8kWOI4enARW2zdzp3GY9IyXSYr_HkZNhogGHxflZBNSXsQJ73PLfUwgkAqujcLGtqSJ_Jw" />

<link rel="stylesheet" href="/assets/frontend/application-a451a77ae29e27908f0002f031ee984039b767565b02703b136a37101a90b2ec.css" media="all" />

<link rel="icon" sizes="48x48" href="/assets/frontend/favicon-24f9fbe064118d58937932e73edafd1d50cb60f7bd84f52308382a309bc2d655.ico">

<link rel="icon" sizes="any" href="/assets/frontend/favicon-d962d21b5bb443f546c097ea21b567cde639adef7370da45be5e349ba8d62d33.svg" type="image/svg+xml">

<link rel="mask-icon" href="/assets/frontend/govuk-icon-mask-cdf4265165f8d7f9eec54aa2c1dfbb3d8b6d297c5d7919f0313e0836a5804bb6.svg" color="#1d70b8">

<link rel="apple-touch-icon" href="/assets/frontend/govuk-icon-180-d45a306f0549414cfa5085f16e4a3816a77558b139e5bc226f23162d1d0decb0.png">

<meta name="theme-color" content="#1d70b8">

<meta name="viewport" content="width=device-width, initial-scale=1">

<meta property="og:image" content="https://www.gov.uk/assets/frontend/govuk-opengraph-image-4196a4d6333cf92aaf720047f56cfd91b3532d7635fc21ebcf0d5897df6b5f77.png">

<script type="application/ld+json">

{

"@context": "http://schema.org",

"@type": "FAQPage",

"mainEntityOfPage": {

"@type": "WebPage",

"@id": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band"

},

"name": "Inheritance Tax: main residence nil-rate band and the existing nil-rate band",

"datePublished": "2016-10-20T16:30:11+01:00",

"dateModified": "2017-06-12T11:34:26+01:00",

"text": null,

"publisher": {

"@type": "Organization",

"name": "GOV.UK",

"url": "https://www.gov.uk",

"logo": {

"@type": "ImageObject",

"url": "https://www.gov.uk/assets/frontend/govuk_publishing_components/govuk-logo-b8553f688131fad665e52a8c2df7633f9cd1c0fffb9f69703cc68c728e7b3b74.png"

}

},

"image": [

"https://www.gov.uk/assets/frontend/govuk_publishing_components/govuk-schema-placeholder-1x1-2672c0fb7a5d5f947d880522c509ebe7f2be090885883cc94418f6860e812e15.png",

"https://www.gov.uk/assets/frontend/govuk_publishing_components/govuk-schema-placeholder-4x3-194fde4197f00e669f6f52c182df2ed707bfb2024c9ef39f7a2ed20da62b90eb.png",

"https://www.gov.uk/assets/frontend/govuk_publishing_components/govuk-schema-placeholder-16x9-30e6c0e035636ee6b9dc72ae254bcd4a925182805afe7c5b7170cf2394894b28.png"

],

"author": {

"@type": "Organization",

"name": "HM Revenue \u0026 Customs",

"url": "https://www.gov.uk/government/organisations/hm-revenue-customs"

},

"mainEntity": [

{

"@type": "Question",

"name": "Who is likely to be affected",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#who-is-likely-to-be-affected",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#who-is-likely-to-be-affected",

"text": "\u003cp\u003eIndividuals with direct descendants who have an estate (including a main residence) with total assets above the Inheritance Tax (\u003cabbr title=\"Inheritance Tax\"\u003eIHT\u003c/abbr\u003e) threshold (or nil-rate band) of £325,000 and personal representatives of deceased persons.\u003c/p\u003e"

}

},

{

"@type": "Question",

"name": "General description of the measure",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#general-description-of-the-measure",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#general-description-of-the-measure",

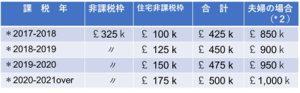

"text": "\u003cp\u003eThis measure introduces an additional nil-rate band when a residence is passed on death to a direct descendant.\u003c/p\u003e\u003cp\u003eThis will be:\u003c/p\u003e\u003cul\u003e\n \u003cli\u003e£100,000 in 2017 to 2018\u003c/li\u003e\n \u003cli\u003e£125,000 in 2018 to 2019\u003c/li\u003e\n \u003cli\u003e£150,000 in 2019 to 2020\u003c/li\u003e\n \u003cli\u003e£175,000 in 2020 to 2021\u003c/li\u003e\n\u003c/ul\u003e\u003cp\u003eIt will then increase in line with Consumer Prices Index (\u003cabbr title=\"Consumer Price Index\"\u003eCPI\u003c/abbr\u003e) from 2021 to 2022 onwards. Any unused nil-rate band will be able to be transferred to a surviving spouse or civil partner.\u003c/p\u003e\u003cp\u003eThe additional nil-rate band will also be available when a person downsizes or ceases to own a home on or after 8 July 2015 and assets of an equivalent value, up to the value of the additional nil-rate band, are passed on death to direct descendants.\u003c/p\u003e\u003cp\u003eThere will be a tapered withdrawal of the additional nil-rate band for estates with a net value of more than £2 million. This will be at a withdrawal rate of £1 for every £2 over this threshold.\u003c/p\u003e\u003cp\u003eThe existing nil-rate band will remain at £325,000 from 2018 to 2019 until the end of 2020 to 2021.\u003c/p\u003e"

}

},

{

"@type": "Question",

"name": "Policy objective",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#policy-objective",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#policy-objective",

"text": "\u003cp\u003eThis measure will reduce the burden of \u003cabbr title=\"Inheritance Tax\"\u003eIHT\u003c/abbr\u003e for most families by making it easier to pass on the family home to direct descendants without a tax charge.\u003c/p\u003e"

}

},

{

"@type": "Question",

"name": "Background to the measure",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#background-to-the-measure",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#background-to-the-measure",

"text": "\u003cp\u003eThe measure was announced at Summer Budget 2015.\u003c/p\u003e"

}

},

{

"@type": "Question",

"name": "Detailed proposal",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#detailed-proposal",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#detailed-proposal",

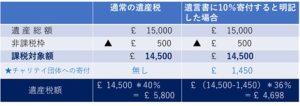

"text": "\u003ch3 id=\"operative-date\"\u003eOperative date\u003c/h3\u003e\u003cp\u003eThe measure will take effect for relevant transfers on death on or after 6 April 2017. It will apply to reduce the tax payable by an estate on death; it won’t apply to reduce the tax payable on lifetime transfers that are chargeable as a result of death.\u003c/p\u003e\u003cp\u003eThe main residence nil-rate band will be transferable where the second spouse or civil partner of a couple dies on or after 6 April 2017 irrespective of when the first of the couple died.\u003c/p\u003e\u003cp\u003eThe nil-rate band will continue to be £325,000 from 2018 to 2019 until the end of 2020 to 2021.\u003c/p\u003e\u003ch3 id=\"current-law\"\u003eCurrent law\u003c/h3\u003e\u003cp\u003eSection 7 of the Inheritance Tax Act 1984 (\u003cabbr title=\"Inheritance Tax Act\"\u003eIHTA\u003c/abbr\u003e) provides for the rates of \u003cabbr title=\"Inheritance Tax\"\u003eIHT\u003c/abbr\u003e to be as set out in the table in Schedule 1 to that Act. The current table provides that the nil-rate band is £325,000.\u003c/p\u003e\u003cp\u003e\u003cabbr title=\"Inheritance Tax\"\u003eIHT\u003c/abbr\u003e is charged at a rate of 40% on the chargeable value of an estate, above the nil-rate band, after taking into account the value of any chargeable lifetime transfers. The chargeable value is the value after deducting any liabilities, reliefs and exemptions that apply.\u003c/p\u003e\u003cp\u003eWhere an estate qualifies for spouse or civil partner exemption, the unused proportion of the nil-rate band when the first of the couple dies can be transferred to the estate of the surviving spouse or civil partner, sections 8A-C \u003cabbr title=\"Inheritance Tax Act\"\u003eIHTA\u003c/abbr\u003e. The nil-rate band can be transferred when the surviving spouse or civil partner dies on or after 9 October 2007, irrespective of when the first of the couple died, so that the nil-rate band can be up to £650,000.\nThere’s currently no specific exemption for a residence, or for assets being transferred to children and other direct descendants.\u003c/p\u003e\u003cp\u003eSection 8(3) to Finance Act 2010 provides for the nil-rate band to be frozen at £325,000 up to and including 2014 to 2015. Section 117 and paragraph 2 of Schedule 25 to Finance Act 2014 extends the freeze on the nil-rate band until the end of 2017 to 2018.\u003c/p\u003e\u003ch3 id=\"proposed-revisions\"\u003eProposed revisions\u003c/h3\u003e\u003cp\u003eLegislation will be introduced in Summer Finance Bill 2015 to provide for an additional main residence nil-rate band for an estate if the deceased’s interest in a residential property, which has been their residence at some point and is included in their estate, is left to one or more direct descendants on death.\u003c/p\u003e\u003cp\u003eThe value of the main residence nil-rate band for an estate will be the lower of the net value of the interest in the residential property (after deducting any liabilities such a mortgage) or the maximum amount of the band. The maximum amount will be phased in so that it is:\u003c/p\u003e\u003cul\u003e\n \u003cli\u003e£100,000 for 2017 to 2018\u003c/li\u003e\n \u003cli\u003e£125,000 for 2018 to 2019\u003c/li\u003e\n \u003cli\u003e£150,000 for 2019 to 2020\u003c/li\u003e\n \u003cli\u003e£175,000 for 2020 to 2021\u003c/li\u003e\n\u003c/ul\u003e\u003cp\u003eIt will then increase in line with \u003cabbr title=\"Consumer Price Index\"\u003eCPI\u003c/abbr\u003e for subsequent years.\u003c/p\u003e\u003cp\u003eThe qualifying residential interest will be limited to one residential property but personal representatives will be able to nominate which residential property should qualify if there’s more than one in the estate. A property which was never a residence of the deceased, such as a buy-to-let property, won’t qualify.\u003c/p\u003e\u003cp\u003eA direct descendant will be a child (including a step-child, adopted child or foster child) of the deceased and their lineal descendants.\u003c/p\u003e\u003cp\u003eA claim will have to be made on the death of a person’s surviving spouse or civil partner to transfer any unused proportion of the additional nil-rate band unused by the person on their death, in the same way that the existing nil-rate band can be transferred.\u003c/p\u003e\u003cp\u003eIf the net value of the estate (after deducting any liabilities but before reliefs and exemptions) is above £2 million, the additional nil-rate band will be tapered away by £1 for every £2 that the net value exceeds that amount. The taper threshold at which the additional nil-rate band is gradually withdrawn will rise in line with \u003cabbr title=\"Consumer Price Index\"\u003eCPI\u003c/abbr\u003e from 2021 to 2022 onwards.\u003c/p\u003e\u003cp\u003eThe legislation will also extend the current freeze of the existing nil-rate band at £325,000 until the end of 2020 to 2021.\u003c/p\u003e\u003cp\u003eIn addition, legislation in Finance Bill 2016 will provide that where part of the main residence nil-rate band might be lost because the deceased had downsized to a less valuable residence or had ceased to own a residence on or after 8 July 2015, that part will still be available provided the deceased left that smaller residence, or assets of equivalent value, to direct descendants. However, the total amount available won’t exceed the maximum available residence nil-rate band. The technical details of how the additional nil-rate band will be enhanced to support those who have downsized or ceased to own their home will be the subject of a consultation to be published in September 2015 ahead of the draft Finance Bill 2016.\u003c/p\u003e\u003ch3 id=\"summary-of-impacts\"\u003eSummary of impacts\u003c/h3\u003e\u003ctable\u003e\n \u003ctbody\u003e\n\u003ctr\u003e\n \u003ctd rowspan=\"3\"\u003eExchequer impact (£m)\u003c/td\u003e\n \u003ctd\u003e2015 to 2016 \u003c/td\u003e\n \u003ctd\u003e2016 to 2017 \u003c/td\u003e\n \u003ctd\u003e2017 to 2018 \u003c/td\u003e\n \u003ctd\u003e2018 to 2019 \u003c/td\u003e\n \u003ctd\u003e2019 to 2020 \u003c/td\u003e\n \u003ctd\u003e2020 to 2021 \u003c/td\u003e\n\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eNil\u003c/td\u003e\n \u003ctd\u003eNil\u003c/td\u003e\n \u003ctd\u003e-270\u003c/td\u003e\n \u003ctd\u003e-630\u003c/td\u003e\n \u003ctd\u003e-790\u003c/td\u003e\n \u003ctd\u003e-940\u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd colspan=\"6\"\u003e These figures are set out in Table 2.1 of Summer Budget 2015 and have been certified by the Office for Budget Responsibility. More details can be found in the policy costings document published alongside Summer Budget 2015.\u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eEconomic impact\u003c/td\u003e\n \u003ctd colspan=\"6\"\u003e This measure could marginally increase demand for housing but it isn't expected to have a significant impact on either house prices or rent levels due to the small overall proportion of the housing market affected and the offsetting impact of wider budget measures. The main behavioural response is the proportion of estates with a residence being left to direct descendants may be expected to increase as people change their wills over time so that their estates can benefit from the main residence nil-rate band to a greater extent. \n\u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eImpact on individuals, households and families\u003c/td\u003e\n \u003ctd colspan=\"6\"\u003e This measure will reduce the burden of IHT for families by making it easier to pass on the family home to direct descendants for all but the largest estates. \u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eEqualities impacts\u003c/td\u003e\n \u003ctd colspan=\"6\"\u003e The government has no evidence to suggest that the measure will have any significant adverse equalities impacts. Those in same-sex relationships may be less likely to have direct descendants, although children will also include adopted and foster children. HM Revenue and Customs (HMRC) doesn't hold data on the protected characteristics of all those potentially affected.\u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eImpact on business including civil society organisations\u003c/td\u003e\n \u003ctd colspan=\"6\"\u003e This measure is expected to have a negligible impact on businesses and civil society organisations. It may lead to a small additional burden for personal representatives to confirm that a residence meets the qualifying criteria. There will be a negligible one-off cost to advisers as they familiarise themselves with the measure and advise on changes that individuals may wish to make to their wills in response to the policy. \n\u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eOperational impact (£m) (HMRC or other)\u003c/td\u003e\n \u003ctd colspan=\"6\"\u003e HMRC will need to make changes to IT systems to deliver changes to the proposals relating to the main residence nil-rate band, the costs of which are currently being finalised.\u003c/td\u003e\n \u003c/tr\u003e\n \u003ctr\u003e\n \u003ctd\u003eOther impacts\u003c/td\u003e\n \u003ctd colspan=\"6\"\u003e Small and micro business assessment: this measure is expected to have a negligible impact on around 25,000 small, medium and micro businesses. Other impacts have been considered and none have been identified.\u003c/td\u003e\n \u003c/tr\u003e\n\u003c/tbody\u003e\n\u003c/table\u003e"

}

},

{

"@type": "Question",

"name": "Monitoring and evaluation",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#monitoring-and-evaluation",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#monitoring-and-evaluation",

"text": "\u003cp\u003eThe measure will be monitored through information collected from Inheritance Tax returns.\u003c/p\u003e"

}

},

{

"@type": "Question",

"name": "More information",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#more-information",

"acceptedAnswer": {

"@type": "Answer",

"url": "https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band#more-information",

"text": "\u003cp\u003eYou can find more detailed information about this change in the \u003ca href=\"https://www.gov.uk/guidance/inheritance-tax-residence-nil-rate-band\"\u003eresidence nil-rate band guide\u003c/a\u003e. If you have any further questions, please contact the \u003ca href=\"https://www.gov.uk/government/organisations/hm-revenue-customs/contact/probate-and-inheritance-tax-enquiries\"\u003e\u003cabbr title=\"Inheritance Tax\"\u003eIHT\u003c/abbr\u003e and probate helpline\u003c/a\u003e.\u003c/p\u003e"

}

}

]

}

</script>

<link rel="canonical" href="https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band">

<meta property="og:site_name" content="GOV.UK">

<meta property="og:type" content="article">

<meta property="og:url" content="https://www.gov.uk/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band">

<meta property="og:title" content="Inheritance Tax: main residence nil-rate band and the existing nil-rate band">

<meta property="og:description" content="">

<meta name="twitter:card" content="summary">

<link rel="stylesheet" href="/assets/frontend/views/_html-publication-2ec7a94cd08f0e5f9e96bab81b496bc9ba1b0b545ec288526689d9539dd9e24c.css" />

<link rel="stylesheet" href="/assets/frontend/views/_csv_preview-bdcc3de538cbb0e5c56fff165b828d91db9bac49da943e57a1c78125e6175327.css" />

<meta name="csp-nonce" content="gccWP/SrylWnTNWYwgaW5Q==" />

<link title="Search" rel="search" type="application/opensearchdescription+xml" href="/search/opensearch.xml">

<meta name="govuk:format" content="html_publication">

<meta name="govuk:publishing-app" content="whitehall">

<meta name="govuk:rendering-app" content="frontend">

<meta name="govuk:schema-name" content="html_publication">

<meta name="govuk:content-id" content="b45c4788-a881-48b4-bcb6-740cc974c2a7">

<meta name="govuk:ga4-base-path" content="/government/publications/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band/inheritance-tax-main-residence-nil-rate-band-and-the-existing-nil-rate-band">

<meta name="govuk:first-published-at" content="2016-10-20T16:30:11+01:00">

<meta name="govuk:updated-at" content="2026-01-09T12:00:52+00:00">

<meta name="govuk:public-updated-at" content="2017-06-12T11:34:26+01:00">

<meta name="govuk:primary-publishing-organisation" content="HM Revenue & Customs">

<meta name="govuk:organisations" content="<D25>">

</head>

<body class="gem-c-layout-for-public govuk-template__body">

<script nonce="gccWP/SrylWnTNWYwgaW5Q==">

//<![CDATA[

document.body.className += ' js-enabled' + ('noModule' in HTMLScriptElement.prototype ? ' govuk-frontend-supported' : '');

//]]>

</script>

<div id="global-cookie-message" data-module="cookie-banner" data-nosnippet="" aria-label="Cookies on GOV.UK" class="gem-c-cookie-banner govuk-clearfix govuk-cookie-banner js-banner-wrapper" role="region" hidden="hidden">

<div class="govuk-cookie-banner__message govuk-width-container">

<div class="govuk-grid-row">

<div class="govuk-grid-column-two-thirds">

<h2 class="govuk-cookie-banner__heading govuk-heading-m">Cookies on GOV.UK</h2>

<div tabindex="-1" class="govuk-cookie-banner__content gem-c-cookie-banner__confirmation">

<div class="gem-c-cookie-banner__content"><p class='govuk-body'>We use some essential cookies to make this website work.</p><p class='govuk-body'>We’d like to set additional cookies to understand how you use GOV.UK, remember your settings and improve government services.</p><p class='govuk-body'>We also use cookies set by other sites to help us deliver content from their services.</p></div>

<p class="gem-c-cookie-banner__confirmation-message--accepted govuk-body" hidden

data-ga4-cookie-banner

data-module="ga4-link-tracker"

data-ga4-track-links-only

data-ga4-set-indexes

data-ga4-link='{"event_name":"navigation","type":"cookie banner","section":"You have accepted additional cookies"}'

>You have accepted additional cookies. <span class="gem-c-cookie-banner__confirmation-message">You can <a class="govuk-link" href="/help/cookies">change your cookie settings</a> at any time.</span></p>

<p class="gem-c-cookie-banner__confirmation-message--rejected govuk-body" hidden>You have rejected additional cookies. <span class="gem-c-cookie-banner__confirmation-message">You can <a class="govuk-link" href="/help/cookies">change your cookie settings</a> at any time.</span></p>

</div>

</div>

</div>

<div class="js-confirmation-buttons govuk-button-group">

<button class="gem-c-button govuk-button" type="submit" data-accept-cookies="true" data-cookie-types="all">Accept additional cookies</button>

<button class="gem-c-button govuk-button" type="submit" data-reject-cookies="true">Reject additional cookies</button>

<a class="govuk-link" href="/help/cookies">View cookies</a>

</div>

<div hidden class="js-hide-button govuk-button-group">

<button

class="gem-c-cookie-banner__hide-button govuk-button"

data-hide-cookie-banner="true"

data-module="ga4-event-tracker"

data-ga4-event='{"event_name":"select_content","type":"cookie banner","action":"closed","section":"You have accepted additional cookies"}' >

Hide cookie message

</button>

</div>

</div>

</div>

<a data-module="govuk-skip-link" class="gem-c-skip-link govuk-skip-link govuk-!-display-none-print" href="#content">Skip to main content</a>

<header data-module="ga4-event-tracker ga4-link-tracker" data-ga4-expandable="" class="gem-c-layout-super-navigation-header">

<div class="gem-c-layout-super-navigation-header__container govuk-width-container">

<nav

aria-labelledby="super-navigation-menu-heading"

class="gem-c-layout-super-navigation-header__content"

data-module="super-navigation-mega-menu">

<div class="gem-c-layout-super-navigation-header__header-logo">

<a class="govuk-header__link govuk-header__link--homepage" data-ga4-link='{"event_name":"navigation","type":"header menu bar","external":"false","text":"GOV.UK","section":"Logo","index_link":1,"index_section":0,"index_section_count":2,"index_total":1}' id="logo" aria-label="Go to the GOV.UK homepage" href="/">

<svg

xmlns="http://www.w3.org/2000/svg"

focusable="false"

role="img"

viewBox="0 0 324 60"

height="30"

width="162"

fill="currentcolor"

class="govuk-header__logotype"

aria-label="GOV.UK">

<title>GOV.UK